The text message landed on the 25th of the month, like it always does: "National Health Insurance premium — ₩146,000 — withdrawn." I'd been in Korea long enough to stop flinching at it, but that month an insurance agent at a coffee shop had just spent twenty minutes telling me I "really should" add a private plan on top. So I sat there with my banking app open and a simple question: I'm already paying into NHIS every month — do I actually need to pay for private insurance too?

I went home and did what I should have done before talking to any agent: I pulled up my actual medical bills from the past two years, read what NHIS does and doesn't cover, and added up the real numbers. This article is the result. If you're a foreigner in Korea wondering whether private health insurance is worth it on top of NHIS, here's the honest breakdown — including the cases where it's a smart buy and the cases where it's money down the drain.

· First, what NHIS already gives you

· The real gaps NHIS leaves behind

· What private (gap) insurance costs and covers

· Who actually needs it — and who doesn't

· Can I opt out of NHIS if I have foreign insurance?

· How to decide in 5 minutes

· Frequently asked questions

First, what NHIS already gives you

If you hold an Alien Registration Card (ARC) and have lived in Korea for six months or more, you are automatically enrolled in National Health Insurance (NHIS) as a local subscriber — it's mandatory, not optional. Many foreigners resent the monthly premium until they actually use it. Here's what that premium buys.

| Item | What NHIS does |

|---|---|

| Coverage share | The government pays roughly 70–80% of the cost for covered treatments. You pay the remaining 20–30% copay. |

| A clinic visit | A typical local clinic (의원) visit often costs you only ₩5,000–₩15,000 out of pocket. |

| Major illness | Serious conditions such as cancer fall under a "special copayment" program (산정특례) that can cut your share to as low as 5%. NHIS does not exclude major illness — that's a common myth. |

| Premium (2026) | Foreign local subscribers pay a floor of about ₩78,000–₩80,000/month, scaling up with declared income and assets. Many mid-career expats land around ₩100,000–₩180,000. |

| Employees | If a Korean company employs you, the premium is split 50/50 with your employer — the cheapest way to be insured. |

So before you buy anything else, understand this: NHIS is genuinely good coverage at a low price. Private insurance in Korea is never a replacement for NHIS — it can only sit on top of it, filling specific gaps. The real question is whether those gaps matter to you.

The real gaps NHIS leaves behind

NHIS is broad but not total. After going through my own bills, these are the places where I — and most expats — actually feel the cost.

1. The 20–30% copay itself

On a ₩50,000 clinic bill, your 30% is trivial. On a hospital stay, surgery, or an MRI, that same 30% can become a meaningful number. NHIS covers most of it, but "most" isn't "all," and a big procedure leaves a real bill behind. (If you've ever priced an MRI here, you know the feeling — I wrote about that separately in "Getting an MRI in Korea: What It Costs.")

2. "Non-covered" (비급여) items

This is the big one. A long list of treatments sits outside NHIS entirely, meaning you pay 100%:

| Often NOT covered by NHIS |

|---|

| Private/upgraded hospital rooms (the difference between a 6-bed ward and a private room) |

| Many physical-therapy and rehab treatments beyond basic limits |

| Cosmetic procedures, orthodontics, teeth whitening, veneers |

| Certain new drugs, premium implants, and elective scans |

3. Income lost while you can't work

NHIS pays doctors and hospitals. It does not put money in your pocket while you're off work recovering. For a freelancer or anyone without paid sick leave, that lost income can hurt more than the medical bill.

NHIS is the floor — it stops any single illness from bankrupting you, and it makes everyday care cheap. Private insurance is the cushion on top — it refunds your copays, pays for the nicer room, and replaces some lost income. You're not choosing between them. You're deciding whether you want the cushion.

What private (gap) insurance costs and covers

The private product most expats consider is often called "gap" or "indemnity" insurance (실손의료보험, silson). It's designed specifically to reimburse what NHIS leaves you to pay.

| Aspect | Typical reality |

|---|---|

| Monthly cost | Roughly ₩20,000–₩60,000 for a healthy person in their 30s. Rises sharply with age and pre-existing conditions. |

| What it reimburses | Your NHIS copays, plus a portion of many "non-covered" bills (with caps and limits that have tightened in recent years). |

| What it won't do | Replace NHIS, cover purely cosmetic work, or pay without limits — recent rule changes cap things like physical therapy and certain scans. |

| Eligibility | Some insurers are cautious about foreigners and short visa terms. Approval and pricing depend on age, health, and visa status. |

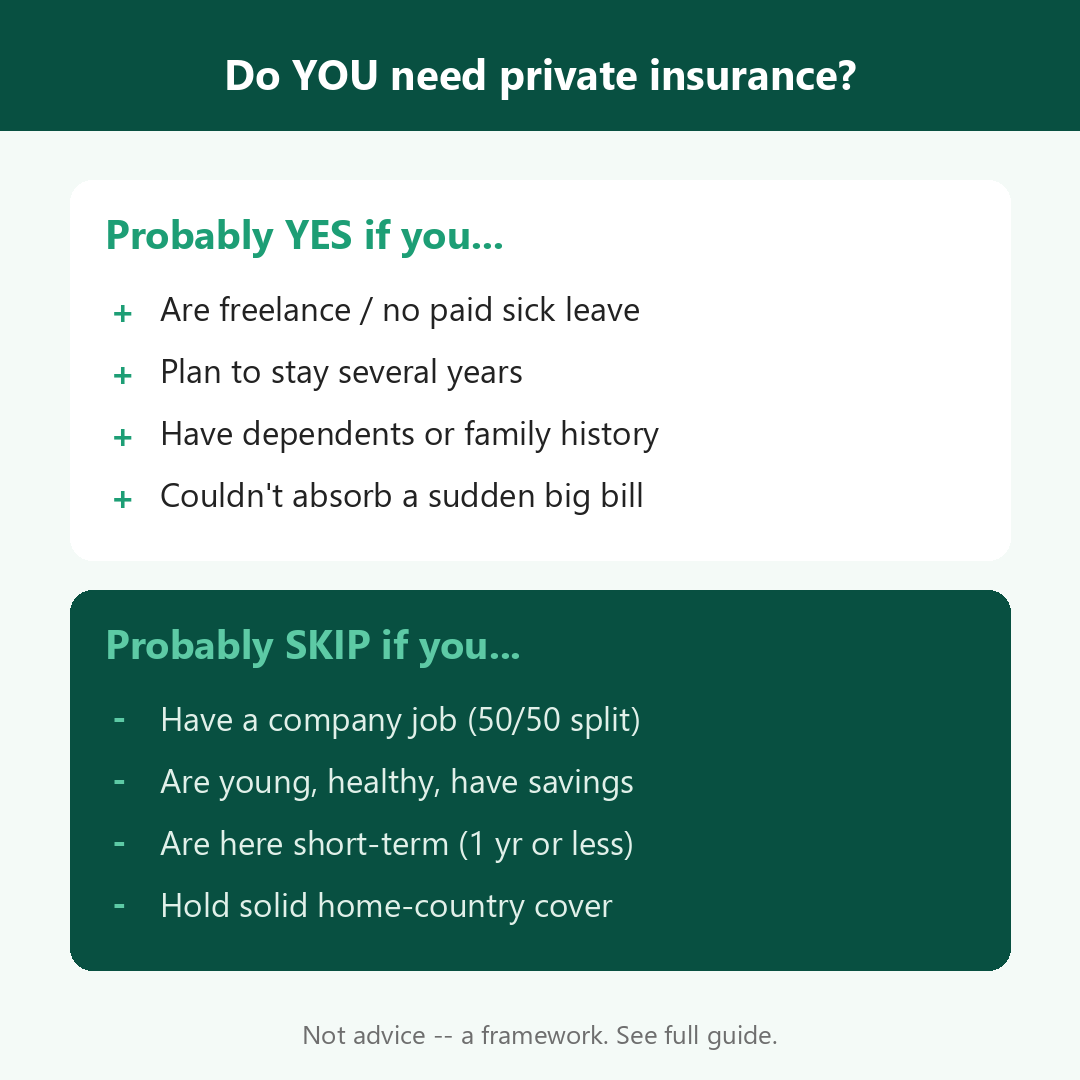

Who actually needs it — and who doesn't

After all the numbers, here's how I'd sort it. This isn't financial advice — it's the framework I used on myself.

Private insurance probably makes sense if you...

You can probably skip it (for now) if you...

Can I opt out of NHIS if I have foreign insurance?

A lot of expats ask this hoping to dodge the premium. The short answer: rarely, and it's gotten much harder. In principle, if you hold an equivalent or superior overseas private policy you can apply to NHIS for an exemption from mandatory enrollment. But since 2019 the criteria have been tightened considerably, and exemptions are seldom granted in practice.

For most foreigners, NHIS is simply mandatory after six months on an ARC — and given how cheap covered care is, "escaping" it usually isn't even in your interest. (If you've ever let a premium slide, be careful: unpaid NHIS bills can create real problems, even at visa-renewal time. I learned that the hard way and wrote it up in "I Ignored My Korean Health Insurance Bills — Then It Almost Cost Me My Visa.")

How to decide in 5 minutes

Frequently asked questions

Q. Is NHIS really mandatory for foreigners?

For most ARC holders, yes — enrollment is automatic after six months of residence, and it's a legal requirement, not a choice. Employees are enrolled through their workplace from the start.

Q. Does NHIS cover cancer and major surgery?

Yes. Serious illnesses are covered, and many fall under a special-copayment program that can lower your share to around 5%. The idea that NHIS "doesn't cover big illness" is a myth.

Q. Does private insurance cover cosmetic dentistry or plastic surgery?

Generally no. Purely cosmetic procedures — whitening, veneers, orthodontics, aesthetic surgery — sit outside both NHIS and standard gap insurance. Medically necessary dental work (extractions, fillings, root canals) is partially covered by NHIS, with you paying roughly 30–50%.

Q. I'm only here for one year. Worth it?

Usually not, unless you have a specific risk. For short stays, NHIS plus savings (or a home-country policy) is often the more sensible mix.

My own answer, in the end: I kept NHIS (no choice anyway), skipped the coffee-shop policy that month, and instead set aside a small "medical buffer" in savings — because as an employee with sick leave, my real risk was low. Your answer may be different, and that's the point. The right move isn't "always buy" or "never buy." It's knowing exactly what NHIS already covers, seeing the gaps clearly, and deciding whether you want a cushion over the floor you already have.

· National Health Insurance Service (NHIS) — Guidance for Foreigners (official English site)

· NHIS foreigner enrollment, premium floor and 70–80% coverage figures — multiple 2026 expat guides

· Gap/indemnity insurance cost ranges and recent reimbursement-limit changes — Korean insurance reporting

· NHIS dental coverage and patient-fee ranges — Korean dental clinic guides

This article is general information for foreign residents in Korea and is not financial, insurance, or medical advice. Premiums, coverage percentages, exemption rules, and private-insurance terms change and depend on your individual income, age, health, and visa status. Confirm current details directly with NHIS (English helpline ☎033-811-2000) and any licensed insurer before making a decision. Figures cited reflect publicly reported ranges as of the publication date and may change.

You already pay into Korea's NHIS every month — so do you actually need private insurance on top? I went through my own bills, the coverage gaps, and the real costs to figure out when private insurance is worth it for foreigners in Korea, and when it's a waste of money.

'건강' 카테고리의 다른 글

| I Ignored My Korean Health Insurance Bills — Then It Almost Cost Me My Visa (0) | 2026.06.18 |

|---|---|

| What Does a Dentist Actually Cost in Korea? (What My Insurance Covered — and What It Didn't) (0) | 2026.06.17 |